Simple Process

How OneBlinc BlincAdvance Works

The entire process takes about 5 minutes — no credit check, no paperwork, no branch visit. Here's exactly how OneBlinc BlincAdvance works from start to finish.

The entire process takes about 5 minutes — no credit check, no paperwork, no branch visit. Here's exactly how OneBlinc BlincAdvance works from start to finish.

From download to cash in your account — about 5 minutes for setup, 2-3 days for standard free delivery.

Search "OneBlinc" on the App Store (iOS) or Google Play (Android). Install the app and create your account using your email and basic personal information. Start your 30-day free trial — no credit card required upfront. If you decide OneBlinc isn't right for you, cancel before day 31 and pay nothing. After the trial, the subscription is $8.99/month flat — the only fee you'll ever pay.

Tap "Connect Bank" and select your bank from the Plaid-powered list of 10,000+ U.S. financial institutions. Enter your online banking credentials — these go directly to Plaid's encrypted servers and are never stored by OneBlinc. OneBlinc's algorithm then analyzes 60 days of transaction history to verify your income pattern and assess your starting advance limit. This process takes 30–90 seconds. No credit check is performed at any point. Your FICO score is completely irrelevant.

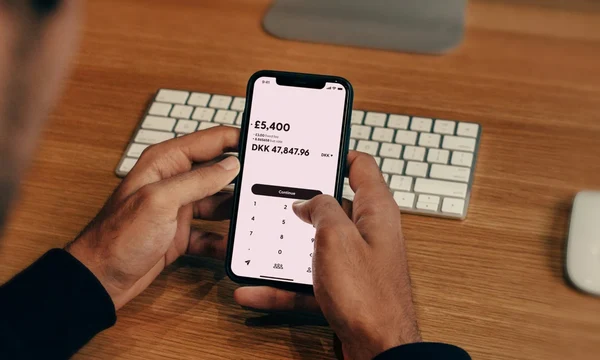

Tap "Request Advance," select your amount ($50–$250 based on your limit), and choose delivery speed. Standard delivery: free, 2–3 business days. Express delivery: $4.99–$9.99, same-day within 15 minutes — available 24/7 including weekends. On your next payday, OneBlinc automatically deducts the exact advance amount from your account. You repay exactly what you borrowed — zero interest, zero late fees.

New users start at $50. Your limit grows automatically with each on-time repayment through OneBlinc's Loyalty Level system.

Many users ask why OneBlinc charges $8.99/month instead of per-advance fees. Here's the honest breakdown — and why the subscription model actually benefits you.

Per-advance fees create a conflict of interest — the lender profits when you borrow more frequently. OneBlinc's flat subscription means BlincAdvance makes the same whether you take one advance or ten advances per month. This alignment of incentives is why BlincAdvance has no hidden fees, no tip prompts, and no upsells. The business model requires active subscribers, not trapped borrowers.

The trial is genuinely free — no credit card required, no automatic billing enrollment. You receive full access to the BlincAdvance feature from day one. You can take an advance, use it, and cancel before day 31 at zero cost. BlincAdvance uses the trial to demonstrate value, not to create billing traps. If you subscribe after the trial, billing begins on day 31 regardless of advance usage.

Only during the 30-day trial. After the trial period, an active $8.99/month subscription is required to request new advances. Your bank connection and account history remain intact if you cancel and resubscribe — you don't lose your loyalty level progress. Resubscribers can request advances immediately after reactivating.

Many Americans aren't comparing BlincAdvance against other apps — they're comparing it against their existing coping mechanisms for cash flow gaps. Here's an honest comparison against the most common alternatives.

| Option | Cost per $200 | Credit Check | Annual Cost |

|---|---|---|---|

| BlincAdvance | $0 + $8.99/month | None | $107.88 |

| Payday Loan | $30–$46 per advance | Soft pull | $720–$1,104 |

| Bank Overdraft | $35 per incident | None | $420 (12 incidents) |

| Credit Card Cash Advance | $5 + 29% APR = ~$7.50 | Hard pull | $90+ (12 advances) |

For Americans using payday loans or paying regular overdraft fees, switching to BlincAdvance is one of the most impactful financial decisions available — with savings of $300–$1,000 per year being common among regular users.

30-day free trial. No credit check. Cancel anytime before day 31 — pay nothing.

Start My Free Trial →